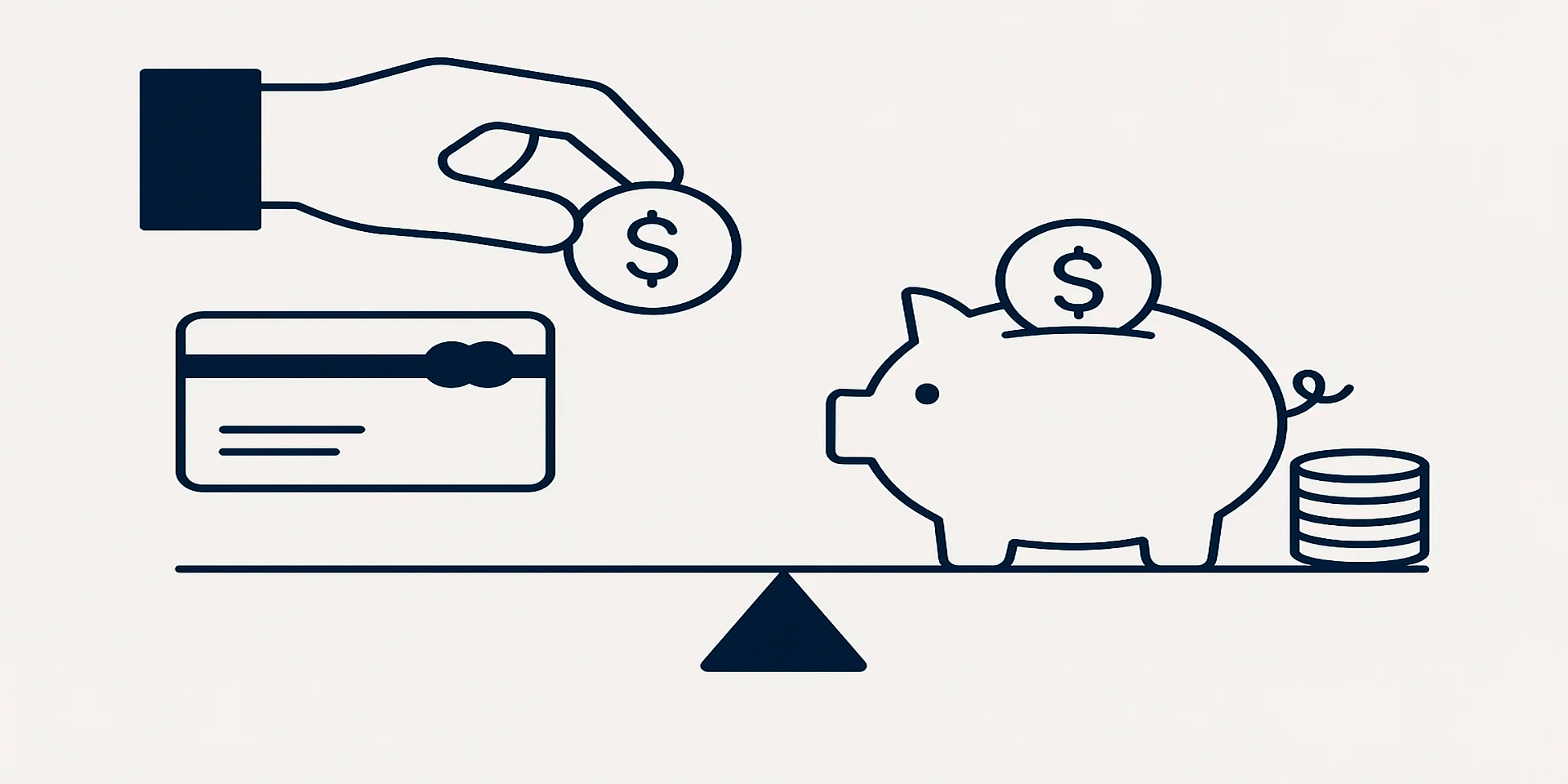

Can Credit Help You Save? Understanding the Trade-Offs

How Credit Affects Your Ability to Save Money

Saving is often presented as the cornerstone of financial security, but credit sits in the same arena, constantly shaping decisions about money. Loans, credit cards, and financing options provide flexibility, yet they also shrink the funds that could be set aside. The link between credit and savings is not black-and-white—it depends on how borrowing is managed, how repayments align with income, and how disciplined individuals are with money. Understanding this push-and-pull reveals whether credit helps build a cushion for the future or quietly drains it away.

The Double-Edged Nature of Credit

Credit creates opportunities that savings alone might not provide. A young worker can lease an apartment, buy a car, or even cover education costs without waiting years to accumulate savings. This accelerates progress but ties future income to debt obligations. Every repayment reduces the amount left for savings. For some, credit becomes a stepping stone toward later financial stability, but for others, it builds a wall of obligations that makes saving an afterthought. The difference lies in how the credit is used and how repayments are structured.

When Credit Enables Savings

Borrowing for education often increases lifetime earnings. A graduate with a degree may repay loans over time while enjoying higher income, which eventually boosts savings capacity. Here, credit does not erase savings—it postpones them until earning power rises.

When Credit Blocks Savings

High-interest borrowing, such as payday loans or revolving credit card balances, leaves little room to save. Instead of building reserves, borrowers focus on keeping up with interest charges. The opportunity cost becomes enormous, as money that could have been saved compounds into lender profits.

Repayment Habits and Their Ripple Effect

The way repayments are handled determines whether credit undermines savings. Timely, consistent payments minimize interest and free up resources for saving. Conversely, missed deadlines cause penalties and ballooning costs, making saving feel unattainable. Repayment behavior is not just about discipline; it reflects planning, awareness, and cash flow management.

Practical Scenarios

A family using credit cards for groceries may plan to pay the balance in full monthly. If they succeed, they preserve cash for savings. If they miss payments, interest grows, eating into the amount that could have gone into their savings account. A renter who consolidates debt into a lower-interest loan frees up income that can be redirected into emergency funds. Repayment style creates these divergent outcomes.

When Credit Becomes a Substitute for Savings

Many households use credit as their fallback when unexpected costs arise. Instead of an emergency fund, they swipe a card or take out a loan for medical bills, car repairs, or temporary job loss. While this provides relief in the moment, it deepens financial vulnerability. Each new crisis adds another layer of debt. Relying on credit as a safety net means depending on lenders rather than one’s own reserves. Over time, the lack of savings magnifies the impact of every disruption, leaving households in a fragile position.

Everyday Examples

A freelancer without savings often turns to personal loans during slow months. The debt fills the gap temporarily but grows if income recovery is delayed. A household that uses a credit card to replace a broken appliance effectively borrows against their future instead of drawing from prepared savings. These examples highlight why credit cannot fully replace the stability of money already set aside.

The Psychological Side of Borrowing

Beyond numbers, borrowing shapes behavior and attitudes. Easy access to credit lowers the urgency to save. Why delay gratification when a purchase can be made instantly with a card? This mindset pushes savings further down the priority list. On the other hand, overwhelming debt creates discouragement, making people feel saving is pointless. Financial psychology is therefore central to understanding why credit can either motivate or obstruct saving.

Building Positive Habits

Borrowers who view credit as a tool rather than a crutch develop healthier habits. They borrow strategically, repay on time, and focus on using debt to strengthen their profile. A strong credit history reduces interest rates on future loans, lowering costs and freeing more room for savings. This positive cycle shows how credit, when managed well, supports rather than sabotages financial goals.

Balancing Borrowing and Saving

The healthiest approach combines both strategies. Credit is used intentionally, aimed at opportunities like education, home ownership, or business growth. Savings are built consistently, even in small increments, to avoid overreliance on debt during emergencies. Balance comes from deliberate planning and habits, not chance.

Steps Toward Balance

- Automate savings transfers so money is set aside before it can be spent on debt or consumption.

- Limit high-interest borrowing that eats into potential savings.

- Match repayments to income cycles to prevent cash flow stress.

- Keep credit usage in proportion to earnings and goals.

These steps ensure that saving grows without being suffocated by repayment obligations. Over time, control shifts from lenders back to individuals, reinforcing stability.

Examples From Real Life

Concrete stories show the tension between credit and savings clearly. A student borrower may spend a decade repaying loans, delaying retirement savings. Yet those same loans unlock career opportunities that increase lifetime wealth. A small business owner who uses credit to expand operations might initially sacrifice savings, but higher profits later rebuild reserves. In contrast, a worker who accumulates revolving debt for everyday spending often finds saving impossible, as interest drains every spare dollar. These real-life cases underline that credit’s effect on saving is not fixed—it depends on context, discipline, and planning.

Generational Perspectives

Young adults often prioritize access to credit over building savings, focusing on establishing independence. Middle-aged borrowers balance mortgages and family costs with the challenge of putting money aside. Older households may avoid credit entirely, relying on accumulated savings to avoid debt. Each stage of life shows a different dynamic between borrowing and saving, but the underlying principle remains: the way credit is managed decides whether savings thrive or vanish.

Conclusion

Credit and savings constantly interact, shaping the financial future of households and businesses alike. Borrowing enables people to act today but often at the cost of tomorrow’s security. When repayments are controlled, credit can support savings by creating opportunities and lowering costs. When unmanaged, it erodes the very money needed for stability. The balance between the two is not about income size but about consistent choices, repayment habits, and the ability to prioritize long-term goals over short-term convenience. By aligning borrowing with disciplined saving, individuals can make these forces work together rather than against each other.